Like clockwork, in times of low interest rates, financial institution executives have questions regarding the changes in their market value results. “What happened to my premium?” they ask. Invariably the answer lies in a little discussed, but oh-so-powerful assumption – the cost of servicing assumption.

Cost adjustments: Wrong assumptions can depress your FI’s market value premium

September 21, 2020

Read Time: 0 min

Key takeaways

- Financial institution executives wondering about changes in their market value premiums might need to look at the assumption used for modeling deposit servicing costs.

- Some ALM models rely on cost of servicing assumptions that haven't been updated in years.

- Ideally, have your own cost of servicing data, but if not, here's a basic formula that might generate more meaningful discussion with your board and ALCO.

Speaking of costs, it is common to see an Economic Value of Equity/Net Value of Equity (EVE/NEV) model assign a cost of deposits to each category of accounts/products. Historically these cost assumptions were from sources that are not easy to find or assess how they were arrived at. For many years, and in many databases today, the source was the Federal Reserve Functional Cost Analysis data that ended in 1991. Of course, that doesn’t make much sense given how much has happened since 1991 in terms of banking delivery costs. Internet and mobile banking are commonplace, unit costs on deposit processing have dropped, electronic statements are the norm, more transactions run through debit cards than paper checks, etc. Why not just keep using the costs from a couple decades ago? I remember that last study well because it included a great big disclaimer indicating that the values were estimates and were NOT to be used when pricing products. Why not? Because the estimates were based on a model that fully distributed all operating costs to a product. The allocation rules were very generic and arbitrary. And besides, it assumed that if you cut a product from your offering lineup, the costs assigned would go away as well. In reality, the only costs that would go away for sure are the direct costs associated with the delivery of the product. The CEO still gets paid. The marketing budget just shifts focus. You get the idea. It’s extremely difficult to assign the cost of these accounts only.

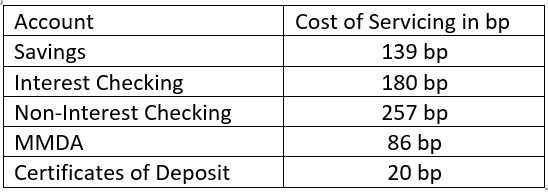

To illustrate the point, below you will find the last Federal Reserve Functional Cost Analysis (FFCA) published costs by products. Note: Much like decay and prepayment rates, these costs are the default costs used in ALM firms for years when institution data is not present.

Servicing costs add to the overall cost of the account like interest expense, raising the all-in cost of the deposit in the market value cash flows.

Servicing costs add to the overall cost of the account like interest expense, raising the all-in cost of the deposit in the market value cash flows.

To arrive at the actual value of the account, we discount each cash flow by a market rate, usually the comparable term FHLB advance rate. When the advance rate is greater than the all-in cost, the deposit has “value” to the institution. When the FHLB rate is lower than the all-in cost, the deposit no longer has value, as the cost of borrowing is cheaper than holding deposit accounts.

In today’s market, the FHLB advance curve shows rates below 1% through 10 years, and between 1.0% - 2.2% on the “long-end” of the curve. Even with low overall interest costs on deposits, adding 86 to 257 basis points quickly takes all deposits values down!

So capturing costs involved with deposit accounts is reasonable enough, and using costs in the calculation of market values is fair. But for many financial institutions, the values we have at our disposal are not reliable or able to be documented. Additionally, the cost assumption should also capture the revenue from non-sufficient funds (NSF) fees, service fees, etc., to accurately reflect the net incremental cost of these accounts.

About the Author